What you Know about YONO?

SWOT analysis of the most popular 'digital bank' of India

YONO (by SBI) is the most popular 'digital bank' of India.

So, what is digital bank?

A digital bank is an online-only off-shoot from an established banking service. It allows you to plan and micro-manage your own finances, but with the support of artificial intelligence, a carefully designed app interface, and powerful data analysis under the hood.

Is a digital bank and neobank the same thing?

The terms are sometimes used interchangeably, digital banks are often the online-only arm of a bigger player in the banking sector, while neobanks are completely digital, existing independently to traditional banks and have no branches you can visit, existing solely online.

Lets come back to YONO.

India's largest bank, State Bank of India (SBI), pulled out YONO - an acronym for 'You Only Need One' - app out of its hat five years ago.

The claimed valuation of Rs 2.94-3.67 lakh crore is more than SBI's Rs 3.25 lakh crore market cap. Though there has been no formal valuation, the number has been derived on the basis of lending book, banking transactions, profitability and potential.

Strength

Huge customer base

with historical data of savings and spends based on which it offers pre-approved loans. The pre-approved personal loan segment that it has grown to Rs 24,000 crore. It is attracting thousands of leads and requests on a daily basis.

According to Sensor Tower, with over 50 Mn downloads on Play Store, the YONO app is now the fifth most downloaded mobile banking or payment app in the world.

YONO Cash

It offers cardless cash withdrawal at ATMs through a one-time PIN. This has been well-received by young customers. The bank is doing around 95,000 cardless transactions a day.

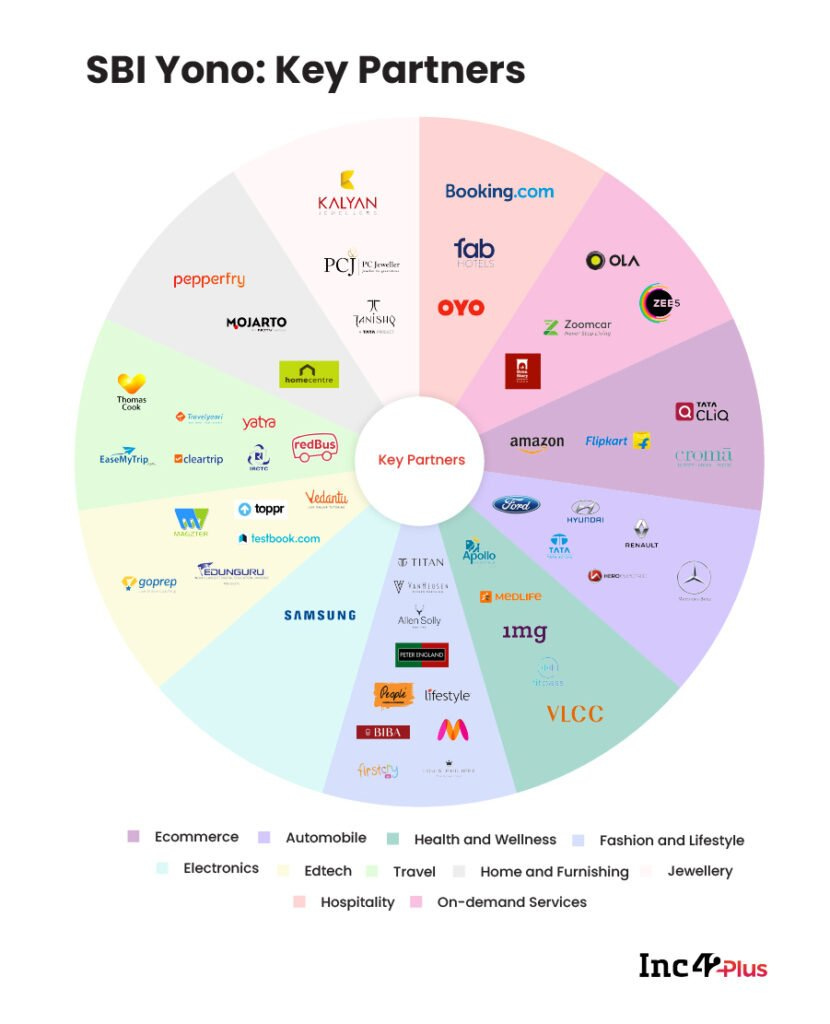

Online Marketplace

Yono has partnered with over 80 ecommerce, agritech, hospitality and other companies in 16+ categories in order to enable the most diverse shopping experience for its consumers.

YONO Krishi

With YONO Krishi, SBI has opened the doors of digital agriculture to farmers. In just one year of its launch, YONO Krishi has disbursed more than 14 lakh Agri Gold loans. It has customised offerings, 15 mandis (online marketplaces) and Mitra (agri information and advisory services).

Weakness

Poor UX

user experience is remarkably poor, as reflected in reviews on Play Store and Apple App Store for the Yono app. It has integrated a series of services that are not typical for banking under the Yono roof. While tapping through the various features of the app, the user keeps getting logged off.

Missing out in addressing Bharat users

A key revenue source for the SBI, government policy implementation has mostly been limited to rural and semi-urban areas only. A major chunk of these account holders either do not own smartphones or are not aware enough in order to be able to use Yono for their personal finance needs.

Opportunity

YONO as a neutral platform

SBI can offer YONO as a neutral platform, without the SBI brand, so that it can be a marketplace for other banks to offer their services. Given that SBI is the largest bank in the country and the PSB space is undergoing consolidation, this will throw up a lot of possibilities for PSB and cooperative banks.

Yono as Future TechFin

Using technology and data, they can offer products that meet their customers' requirements, engage more often and provide a superior banking experience. New technology-led offerings and close knowledge of the customer will add to the customer stickiness.

Threat

Neobanks and fintech apps

Banks share their banking APIs with neobanks and fintech apps but they don’t share their banking APIs with other banks. As a result, they are able to track all the accounts of a consumer have conclusive data with regards to a consumer, more than what a bank may have. This allows them to extend value-added features and products based on the data, including loans.

Source: -

https://thegate.boardingarea.com/the-most-popular-digital-bank-in-almost-every-country-in-the-world/

https://inc42.com/features/explained-behind-the-sbi-yono-hype-the-40-bn-question/

https://www.businesstoday.in/magazine/finance/story/yono-sbis-start-up-299520-2021-06-24

Views expressed are personal. Please be free to give your suggestions/inputs or counter-arguments. I will be happy to discuss them. You can follow me on LinkedIn or Twitter